On the Pension Apocalypse

Aging populations, archaic pay-as-you-go systems, and undercapitalized pension funds will create huge problems for future retirees. Just how bad is it, and what should you do about it?

The Situation

In the past there were many workers and few retirees, so it seemed like a good idea to have the workers pay for old peoples' pensions and promise them the same in return. Thus the pay-as-you-go pension system was born.1 But people stopped having children, started living longer, and the worker:retiree ratio has been falling and will continue to fall precipitously. These problems will be coming home to roost over the next few decades.

{kind=link}

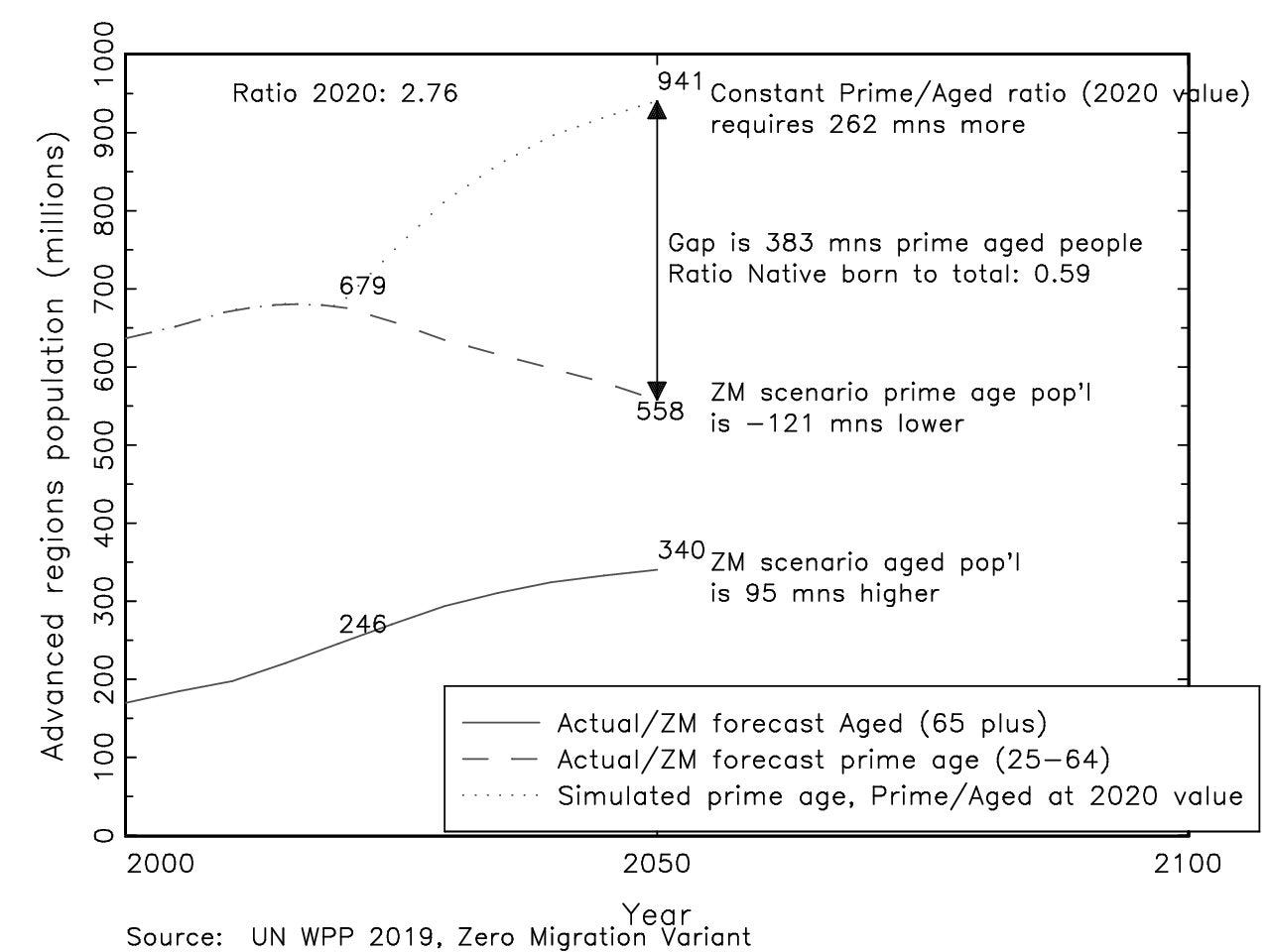

To put things into perspective: simply maintaining the current prime:aged ratio would require 383 million additional prime aged people by 2050. The math is clear, and even if fertility tripled tomorrow morning there's a huge lag until that actually starts affecting the economy.

How much will it cost? It's hard to say exactly, the projections depend on fertility, longevity, immigration, growth, and the actual pensions. Plus there are non-pension expenses to take into account: government-funded healthcare spending on retirees is going to increase as well. On the low end some (including the EU) project an increase in spending of just ~3% of GDP, but I find that highly implausible. My own forecast would be around 10% of GDP for the average advanced economy by 2050.

For countries with relatively low government spending and good growth prospects like the US this might not be a problem. For European countries that already have government spending in the 55%+ of GDP range however, things look dire.2 Raising an additional 10% of GDP through taxation would result in a 20-25% cut in disposable income for the average worker for literally nothing in return. Combine that with low/zero growth and things start looking really bad.

Anyone under the age of 40 or so should expect to receive little in return for their pay-as-you-go pension system contributions. Is it unfair that today's workers slave away, are forced to give away all their money to the boomers, only to receive virtually nothing in return? Sure. Is there anything you can do about it? No. Welcome to democracy.

Regional Variation

There is enormous variation in pension systems both between and within countries. Places with relatively small pay-as-you-go systems and heavy reliance on private pensions are probably going to be fine. On the other hand there are municipalities in the US which have already started defaulting.

EU

By 2050, the German workforce is expected to shrink by about 10 million people while the number of retirees will increase by about 7 million people. Most European countries should expect little to no GDP growth in the coming decades, as workforce declines will offset productivity gains. And most of Europe isn't seeing any productivity gains anyway (though some countries, such as Germany, have been growing):

Even more terrifying is the fact that nobody really seems to care about growth in Europe. There's this idea that the EU is ruled by technocrats, but these "technocrats" seem more concerned with adding annoying popups to every website than the permanent collapse of economic growth in the European Union.

Japan has had zero GDP growth since 1995 (which was also when its workforce was at its highest point), and Europe should expect a similar future. Here's what the Nikkei 225 has looked like over the past 3 decades, by the way:

The pie is no longer growing; all that's left is the fight over who gets the biggest piece. Sam Altman is right when he argues that zero-sum economics create a toxic political environment.

In a system with economic growth, things can improve for everyone. In a system without growth, or even one with very little growth, that’s not the case—if things improve for me, it has to come at the expense of things getting worse for you. Without growth, we’re voting against someone else’s interest as much as we’re voting for our own. This ends with lots of fighting and everyone feeling screwed, broken into factions, and unmotivated. Democracy does not work well in a zero-sum world.

People either seem unaware or incapable of preparing for what is to come. Even in prosperous countries like Germany and France, median savings are below €100k. The wealthiest German cohort, those aged 55-64, have median net wealth of €180k, and the younger generations don't seem to be in a hurry to save for retirement. 42% of Europeans have less than three months’ take-home pay saved.

Japan

Despite being ahead of the curve on aging, Japan is actually in a pretty good position as it only spends ~10% of GDP on pensions. Compare that to 17% in Italy, 14.5% in France, and 10% in Germany even though those places have significantly smaller retired populations.3 How do they do it? It's a pay-as-you-go system that simply doesn't pay out very much: the average pension is only ~$2k per month for a married couple. Could you live on that budget? Despite this, they are cutting pensions, increasing the retirement age, and finding ways to get older people to keep working.

It's also worth mentioning, however, that they've been running deficits for 30 years and have a debt/GDP ratio of over 230%. Total government spending has been hovering around 40% lately, so it would seem that they have room to increase taxes if it becomes necessary.

China

China is in a nightmarish demographic position and needs to maintain rapid growth despite a declining workforce. Their age pyramid is a time bomb that's about to explode:

In 2011, every pensioner was supported by 3.1 workers. By the end of 2017, that ratio had fallen to 2.8-to-one, and the Ministry estimates that by 2050, it will be just 1.3-to-one.

In 2016 the one-child policy became the two-child policy. In 2021, the two-child policy became the three-child policy. But it's too late.

How long can China keep up the "outgrow the debt" strategy with a declining workforce? And what happens when growth stalls? This seems like one of the likelier scenarios for the next global recession. Of course many have predicted this collapse before, and they were wrong. But the demographic problem is unavoidable.

The retirement age is quite low: 60 for men and 55 for women; we can probably expect this to change which will give them a bit of breathing room. But any such changes are wildly unpopular. On top of that, pension funds are already heavily reliant on additional funding from the central government.

USA

Given its low average age and strong growth, the US is in a decent position compared to the EU and China.

But there is a large amount of variation within the country: some local governments are doing perfectly fine, while others have serious problems with defined-benefit pensions for public employees. Politicians have been promising generous pensions without bothering to fund them (with the assistance of absurd return assumptions from the funds): pensions give them the ability to offer huge payouts to special interest groups without impacting the budget immediately. The logic of public choice is so clear that there is only one really serious question left, and that is why states haven't collapsed already.

As these pensions start taking up a larger percentage of state/local revenues, things will come to a head. In Illinois, for example, pensions took up about 4% of the budget in the 90s. Today it's 25% and growing. There are three alternatives, all painful: cut pensions, cut other services, or start raising taxes. How much of that will people tolerate before they start moving out?

If this were simply a horrific problem that we were trying to deal with, it would be bad enough. But it's a horrific problem that we are ignoring, and will continue ignoring until it blows up in our faces. In the middle of the longest bull market in US stock market history, pension deficits have ballooned:

Just imagine what a decade of weak stock market returns would do.

At the federal level, Social Security has about 15 years until they have to start cutting benefits, but it won't be that expensive to shore it up. And most importantly, the US is growing, and has a lot more room left for tax increases.

What Governments Can Do

How will governments respond to the pension apocalypse? All the alternatives seem bad: pension cuts, big tax increases, vast borrowing, inflation, unprecedented immigration. Nobody wants to do any of these things, but the math must eventually balance out. In the end something's gotta give. This survey of Europeans captures the heart of the problem:

When it comes to the measures required, even those respondents who acknowledge the threat of demographic problems appear to be fairly reluctant to endorse them: most of the reform proposals are refused by the majority.

Everyone understands that governments either need to tax more or pay out less, but people aren't ready to accept either solution. Just 46% support a system that combines basic public pensions with private savings! Even conservatives in America hate the idea of cuts: just 15% of Republicans support Medicare spending cuts, while 10% support Social Security cuts. And when you spend $2T on "stimulus" at a time when there is no AD shortfall, how are you going to close the taps later? With such large political costs (old people are sympathetic, numerous, and politically influential),4 few politicians are willing to take the necessary steps. And the worse the worker:retiree ratio, the more political power the retirees have—this is not a self-balancing problem.

The example of Japan shows that these problems are not insurmountable, as long as politicians are willing to make difficult choices (and the people accept those choices). The earlier reforms are enacted, the easier things will go, but in most places I expect it will be impossible until a breaking point is reached. Maybe in the end we'll just get a little bit of everything and the math will balance out. But someone is going to have to make sacrifices.

The biggest danger comes not from the pension apocalypse itself, but rather from the stupid things politicians might do to avoid addressing the pension problem head-on. Some possible scenarios:

Huge tax increases → mass emigration → death spiral

Central banks monetize debt → hyperinflation → economic crash

Central banks don't monetize debt → debt crisis → Greece 2.0

Grow

You can think of pension liabilities like debt: you can keep growing it forever without problem as long as you also grow your economy quickly enough. We can talk about progress studies as much as we want, but the practical reality on the ground is not encouraging when it comes to growth. Especially in Europe, it is more or less a distant dream rather than a real possibility. And things are slowing down even in the US.

China has no alternative, and so far it seems to be succeeding against all expectations (though the data is fake to some extent, see this and this). We'll see how long they can keep it up.

Pay Out Less

One possibility is, of course, a straight cut to pensions. But you have to keep in mind that old people tend to vote at higher rates than young people, and that due to demographic collapse the old people will be the most powerful voting block in these countries. People get angry when you cut spending.5 They get especially angry when they have paid in quite a lot of money to the pension system and will not see much in return. Even the best-managed systems (like the Dutch) will be running into trouble though.

Raise the Retirement Age

Instead of paying out less, you can try to raise the retirement age instead. This not only decreases the total amount you need to pay, but also props up the worker:retiree ratio. It also has the benefit of not affecting current retirees: bypassing that powerful bloc makes changes easier to implement from a political perspective. But people in surveys say they expect to retire around 63, so I don't know how politically viable this plan is going to be in practice.

For example, Denmark plans to raise the retirement age in step with increases in life expectancy. Under this model, a Danish worker born in 1990 can expect "early retirement" at 70 and normal retirement at 73!

To which I say: fuck off and die.

Edit: after some conversations I have decided that raising the retirement age might not be that bad. Lots of people are still able and willing to work in their 60s and 70s. The best solution would probably be a flexible system in which people can choose when to retire, and the benefits adjust accordingly (the earlier you stop working, the less you get).

Tax

Raising taxes is another possibility, but how much slack is there in income taxation given a declining base? The US (which is currently at <40% government spending/GDP) has a lot of wiggle room, and you could even say the same about China. But for Europe you have to figure that at some point they'll be hitting the downward slope of the Laffer curve. Emigration is easier than ever and the people with the greatest ability to work remotely also tend to be those who are most desirable from a fiscal perspective.

Immigration

The sheer number of people needed makes immigration a partial solution at best, and only a few countries use immigration in a way that actually helps. Canada, New Zealand, Australia, and Switzerland for example have fairly reasonable immigration policies that select for high human capital: Canada has the smartest immigrants in the world (average PISA math scores of 527, higher than the natives' and corresponding to an IQ around 103). But despite high population growth and productive immigrants, Canada still faces a shortfall in the near future.

Needless to say, immigration policies that select for low human capital (US: average 1st gen immigrant PISA math score 437, corresponding to an IQ around 91) only make the problem worse. In Europe, non-EU migrants are less likely to be employed and earn much less than Europeans when they are employed. You can't fill a fiscal hole by adding more fiscal burdens to your society.6

There is astonishingly little international competition for productive people, but I think that is going to change in the future. This process has already started, with some countries offering digital nomad visas, sometimes with tax incentives on top. In Italy some cities will pay half your rent. I imagine there will be calls for coordination to prevent a "race to the bottom", but I doubt there will be any kind of global agreement on the matter.

Debt

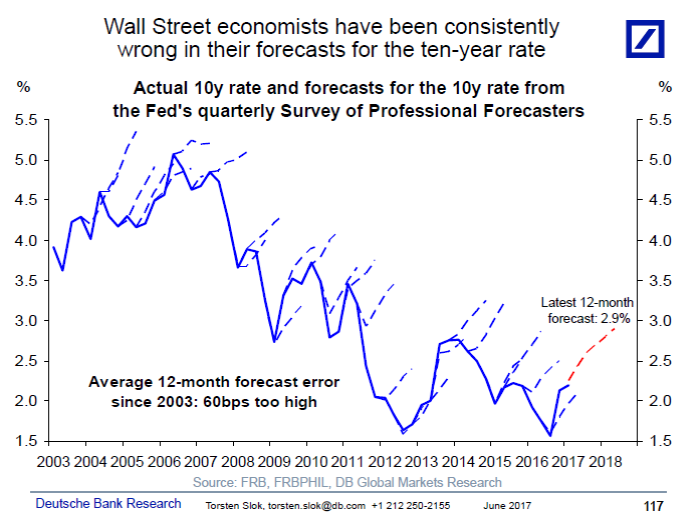

Hell, if zero rates persist you could just fund the whole thing with debt. Rising interest rate forecasts have been a complete meme for more than a decade now, maybe free money is the new normal. On the other hand, at high levels of debt/GDP it only takes a small rise in rates to create serious problems (and possibly trigger debt crises). But how long can this last? Perhaps the "solution" to rising rates will be inflation, just kicking the can even further down the road.

{kind=link}

The Andrew Dobson Gambit

Inflate!

How much willingness for debt monetization is there among independent central banks? Probably not much (who knows though—remember "no bailouts"? lol) On the other hand, how long can CBs retain their independence against mounting political pressure? What's more unpopular, high inflation or pension cuts? This seems like a fairly unlikely scenario.

Transition to DC Plans

The countries that are best prepared have some combination of well-funded basic public pension system that makes sure old people don't starve, combined with defined-contribution pensions. Governments with large defined-benefit plans will either need to take serious pain, or start transitioning to defined-contribution plans. The problem with making this transition is that it's expensive immediately, and extremely difficult politically. They tried to do it in Illinois and it was shot down by the courts:

Under the Illinois Supreme Court’s 2015 precedent, a government worker’s pension benefits cannot be changed in any way after their first day working for the state.

If you thought pensioners were a powerful lobby, wait till you see what public employees get away with.

What You Can Do

First of all, understand that you need to save for retirement.

After that, just follow the standard boring investing advice. Right now is not a great time (high valuations after a 12-year bull market that quintupled the S&P500, near-zero bond yields), but I'm sure there will be good opportunities in the decades to come. The safe withdrawal rate (how much you can withdraw from your investments every year without running out of money before you die) is generally held to be around 3-4%. Suppose you can get by on $30k/year, you'll need $1m in investments. That number has to be adjusted for inflation: assuming you'll retire in 2060 and 2% inflation, that's $2.2m in 2060-dollars. Getting there isn't that difficult: saving $10k/year for 40 years with 7% annual returns will get you to $2m. The earlier you start the better.

Where to put the money? I'd go with some sort of global equity ETF, perhaps with a tilt toward the US. Beware home equity bias, unless you're American.

What happens if the political demands generated by the collapse of pension systems end up causing a hyperinflationary scenario? As long as you have the money in real estate or equities, you'll probably be fine. German stocks actually did fine in the Weimar hyperinflation era (but only if you held them through an 80% drawdown).

It's an absolutely terrible time for bonds, don't be misled by the incredible bull market of the last 40 years. 60/40 is going to look much worse in the future. Inflation goes up, you're screwed; rates go up, you're screwed. The Greek 10y bond is currently yielding 0.824%—this is a country with a debt/GDP ratio over 200%, a GDP 35% lower than it was 10 years ago, and a recent history of default. The bond market is absolutely nuts right now.

If things get bad enough you might want to protect against expropriation, which means international diversification. But I doubt things will get that bad.

Looking beyond investments, you could move to a cheaper country, which would allow you to get away with lower savings. There are nice places in SEA or South America that are both civilized and cheap. It's pretty easy for Norteamericanos and Europeans with some savings to get retiree visas. If you were retiring now, Argentina would be an interesting choice: very cheap due to the currency situation but still a safe & pleasant country. As long as your investments are in a stable currency, you can go wherever you want. On the other hand your home country might be unwilling to pay out even your meager pension if you don't actually live there, so plan accordingly.

You could also have more kids. The society-wide dependency ratio is going to be pretty bad, but if you have enough kids your family dependency ratio could be relied on instead. It's probably a bad idea to have kids as a retirement strategy, but if you're leaning in that direction already why not read Caplan's book and pop out another one?

What to Expect

Some countries have a political culture that allows for tough decisions to be made and accepted, but for everyone else I think the most likely course is to kick the can down the road and muddle along while the problems accumulate, until a crisis erupts.

Worst-Case Scenario

Weimar, then war? Probably not. Societies filled with old people don't do revolution or war. The age of bangs is over; we only have whimpers to look forward to. At worst we'll see a death spiral of stagnation, brain drain, expropriation, and perhaps devaluation/inflation. Think South America. They won't let you starve, but it won't be very nice either. If the catastrophe isn't global, and you manage to keep your portfolio out of their hands, you'll be fine.

Best-Case Scenario

Cheap fusion energy or friendly superhuman general artificial intelligence?7 If we get a significant increase in growth, the pension problems disappear.

I believe the first such system was set up in Germany in 1889.

They could theoretically cut spending on other things to compensate, but good luck with that.

In Japan 28% of the population is >65 years old. That number is 23% in Italy and 21.5% in Germany.

When 30%+ of the population is retirees, nobody's getting elected without their vote.

"Expenditure cuts carry a significant risk of increasing the frequency of riots, anti-government demonstrations, general strikes, political assassinations, and attempts at revolutionary overthrow of the established order. [...] Once unrest erupts, governments quickly reverse course and increase spending in the following year".

European immigration policy is such a mystery to me it might as well be a supranatural phenomenon. In the US at least you can explain it through the political motive. But what about Germany? Poor, unemployed migrants obviously don't vote CDU. If there is any intentionality at all behind European immigration policy (and there probably isn't) it must be based on a fundamental misunderstanding of how the welfare state works.