Returns to Scale in Broken Windows

Everyone is familiar with Bastiat's broken window fallacy: breaking a window may seem to generate economic activity through its repair, but it's actually a loss once you take the opportunity cost into account. But what if there were positive returns to scale in breaking windows? There is a fascinating subgenre of economic research which involves looking at large-scale destruction, analyzing the long-term effects, and then concluding that the disaster was Good, Actually.

Let's take a look at some examples.

Raze the cities

You must be ready to burn yourself in your own flame; how could you rise anew if you have not first become ashes?

We'll start with Hornbeck & Keniston's Creative Destruction: Barriers to Urban Growth and the Great Boston Fire of 1872. The titular fire destroyed 776 buildings (about 1/10th of Boston's housing stock at the time), and caused ~$13 million in damages to real estate and ~$60 million in lost personal property. Thirteen people died.

After the fire, there was a significant increase in land value in the burned area, which the paper attributes to positive externalities from investing in new buildings. Prior to the fire, negative externalities from other, low-quality, buildings prevented high-quality development; the coordination problems were too difficult to overcome. Mass destruction and rebuilding let the areas settle at a higher equilibrium. Crucially, the value gain is estimated to be larger than the value of the destroyed buildings:1

The Fire is estimated to have increased land values by $5.3 million in the burned area, and by $9.0 million in the unburned area. The percent impact is greater in the burned area, but the level impact is greater in the unburned area because many more plots are affected. The estimated total impact is $14.3 million, or 1.12 times the 1872 value of buildings in the burned area.

(And you could argue that the value of the land doesn't fully capture the gains here.)

Importantly, there is no such land-value gain in situations where individual buildings burned down. It is only when destruction happens at scale that reconstruction can happen in new and more profitable configurations, because the limiting factor is externalities and coordination. Break one window and all you get is a broken window; break a ton of windows and all sorts of new possibilities emerge. The paper is not clear on the exact mechanism, but the authors speculate that it's some combination of combining plots into larger parcels, concentrating land ownership and reducing coordination costs, improved infrastructure, agglomeration gains from improved business locations, and displacement of businesses that caused negative externalities on neighbors.

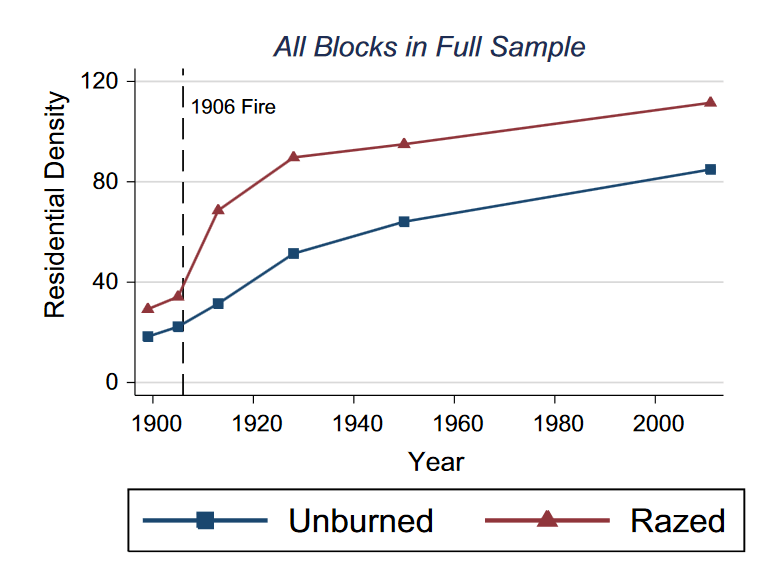

Another paper along the same lines is Siodla's Razing San Francisco: The 1906 disaster as a natural experiment in urban redevelopment, which finds that the fire increased density by 60%. In a wildly prosperous city which used to be fast-growing but whose population has stagnated for the last 70 years, 60% is incredible. The key takeaway here is that mass destruction enables not just higher-value uses, but also very different forms of reconstruction.

After the fire, developers constructed much denser housing in razed areas relative to unburned areas where frictions were still in place. This result is consistent with the notion that the frictions associated with adjusting land use in cities are substantial, even in relatively free-market ones.

Whether the effect persists to this day or not is questionable: with the addition of various controls, it disappears by 1950, but I'm not sure which specification we should be looking at. Part of the issue is that modern-day redevelopment erases the positive effects of the fire.

As Christine Meisner Rosen puts it in The Limits of Power: Great Fires and the Process of City Growth in America,

Prior to the fire, the manner in which improvements had been erected on the land acted as a constraint to redevelopment. The razing of the extant buildings gave rise to the possibility that the burnt area could be redesigned as it was rebuilt.

Fire isn't the only way. Bombing offers similar benefits, as Dericks & Koster show in The Billion Pound Drop: The Blitz and Agglomeration Economics in London. I love everything about this paper, right from the first sentence which includes the golden words "exogenous variation from the Blitz bombings".

This one isn't about residential density, but rather about employment density and agglomeration effects. There are economies of scale external to individual firms: knowledge spillovers, labor market effects, possibilities for specialization along the supply chain, etc. All these make the tight clustering of economic activity valuable. Dericks & Koster show that bombed locations tend to have increased building height today, and that higher density leads to greater gains from agglomeration. They estimate that the blitz led to an increase in current-day per capita income of almost 10%! That's about £50 billion per year.

When people talk about the long shadow of history, I don't think London's employment density is exactly what they have in mind, but that just goes to show how little attention we pay to zoning relative to its importance. The implications for transaction costs are also rather shocking: the value unlocked by these disasters is enormous, yet Coasean bargains in normal times seem impossible.

How much of these effects can we blame on regulation? It's not clear, some of it is just organic externalities which are naturally difficult to coordinate against, so I think we would see similar situations even under a laissez-faire zoning regime. On the other hand, as zoning regulation has proliferated perhaps the positive effects of mass destruction would be muted today. That said, a controlled demolition would cause far less damage compared to unpredictable destruction from fires or bombs: people and movables would be safe, and only the buildings would be lost.

Natural remedies

Whoever must be a creator always annihilates.

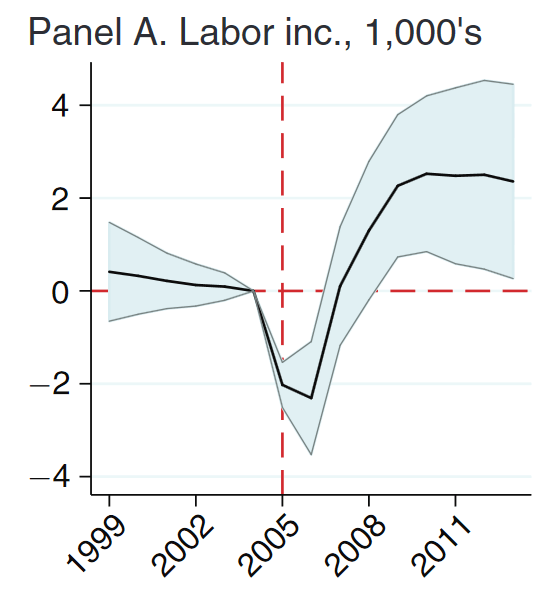

What about floods, hurricanes, or earthqukes? Let's turn our eyes to Deryugina, Kawano & Levitt's The Economic Impact of Hurricane Katrina on Its Victims: Evidence from Individual Tax Returns. Hurricane Katrina hit New Orleans in 2005 and destroyed over 200k homes, mainly from flooding as the levees failed. Hundreds of thousands of people were permanently displaced, and the damage was estimated to cost over $100 billion. Based on comparisons against a control group of 10 similar cities, they find that relative incomes initially decreased, but then quickly recovered and kept increasing beyond their original level.

The gap in income increases to about $2,300 in the following year but, remarkably, disappears just two years after the storm. By 2008, labor incomes are $1,300 higher among the New Orleans group; this difference exceeds $2,300 by 2013.

The income gains in this case (about $1.8b between 2005-2013) were not sufficient to make up for the losses due to the flooding, but again this is mainly due to the unpredictable nature of the destruction, and it shows that output is incredibly resilient to disasters. Others find, if not a stimulating effect, then at least a quick return to pre-disaster levels of output.

This rebound appears to be driven both by victims moving to stronger labor markets and by the strengthening of the labor market in New Orleans itself. What makes the strong economic recovery even more remarkable is that the storm struck without warning. In settings where economic agents have more time to prepare for adverse events (e.g., long-term climatic changes that make an area less habitable), the adjustment costs would be expected to be lower.

For a broader view of natural disasters, we have Skidmore & Toya's Do Natural Disasters Promote Long-Run Growth? which looks at cross-national data. It's not the most convincing paper in the world: they find that climatic disasters tend to promote growth, while geologic disasters tend to slow it down, and the proposed mechanism (greater disaster risk -> more human capital investment -> greater growth) strikes me as rather dubious.

Thus, physical capital investment may fall, but there is also a substitution toward human capital investment. Disasters also provide the impetus to update the capital stock and adopt new technologies, leading to improvements in total factor productivity.

Go to war, have a revolution

War has always been the grand sagacity of every spirit which has grown too inward and too profound; its curative power lies even in the wounds one receives.

While the previous cases have relatively clear mechanisms, war is a bit different. Its positive effects—if they exist—are more diffuse in their operation. Military R&D investments filtering down into the economy, efficiency improvements from the impetus of the war economy, and so on.

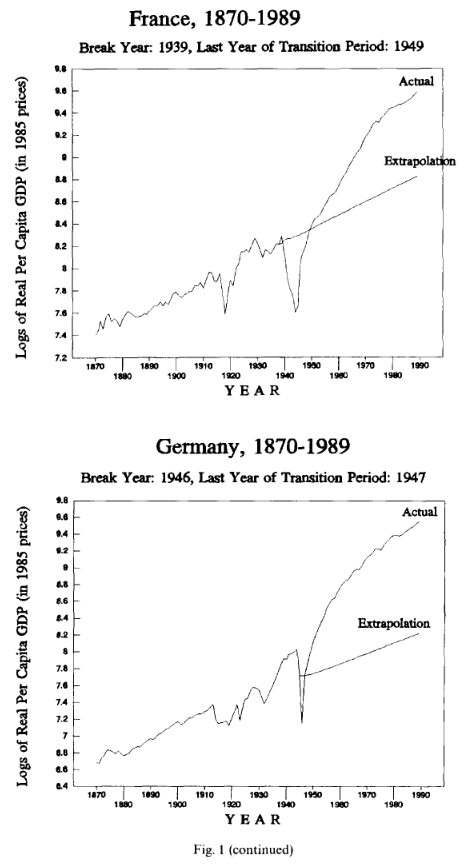

Ben-David & Papell look at 16 countries and find that growth following WWII more than doubled, even after GDP levels surpassed the pre-war path. Per-capita growth rates are 163% higher than the pre-break rates.

You don't even have to win the war to get the benefits.2

This study provides empirical evidence that, for nearly every one of the countries, the years that provide the strongest evidence for a trend break are associated with a sharp decline in GDP. These breaks are associated with World War II for most of the countries and either World War I or the Great Depression for the remainder. While countries do tend to exhibit relatively constant growth rates for extended periods of time, the occurrence of a major shock to the economy and the resultant drop in levels are usually followed by sustained growth that exceeds the earlier steady state growth.

Robert Gordon makes a similar argument in The Rise and Fall of American Growth, arguing that the necessity of the war effort forced TFP increases onto the entire economy, spilling out of the military and onto the civilian sector. Even Tyler Cowen has made arguments along these lines, writing that "the very possibility of war focuses the attention of governments on getting some basic decisions right — whether investing in science or simply liberalizing the economy. Such focus ends up improving a nation’s longer-run prospects." (Though he does not go as far as to say war is a net positive.)

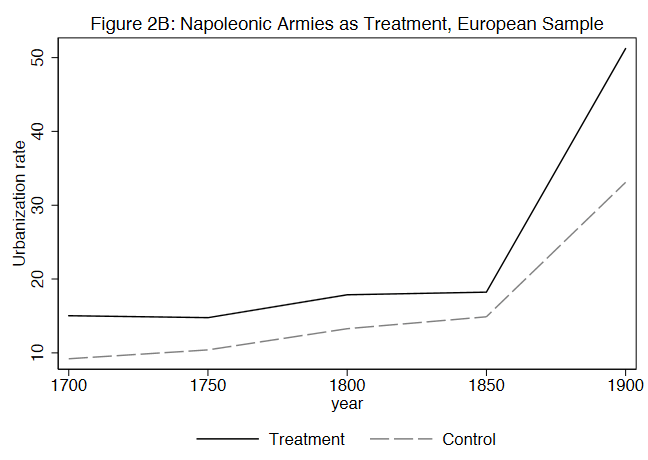

On the revolution side there's Acemoglu et al's The Consequences of Radical Reform: The French Revolution. At this point you can probably guess what they found:

Areas that were occupied by the French and that underwent radical institutional reform experienced more rapid urbanization and economic growth [...] Revolution destroyed (the institutional underpinnings of) the power of oligarchies and elites opposed to economic change; combined with the arrival of new economic and industrial opportunities in the second half of the 19th century, this helped pave the way for future economic growth.

The success of the French reforms raises the question: why did they work when other externally-imposed reforms often fail? Most likely this is because the reforms were much more radical than is typically the case.

And then there's the Branko Milanovic thesis that communism was necessary for eventual capitalist development in Eastern Europe.

I mentioned Mancur Olson's Rise and Decline of Nations in the Gibbon review, and I have to bring him up again here. Olson's argument is that in the long run nations decline because they accumulate cruft in the form of rent-seeking special interest groups. The rest is downstream from the logic of public choice. A war or a revolution can wipe the slate clean and thus revitalize the economy. The Acemoglu paper fits into this framework very well, as Napoleon destroyed rent-extracting institutions like guilds.

Perhaps we should not simply raze the cities, but wipe out all our institutions as well. What we need is a big fat societal 'reset' button.3 Olson, of course, is equivocal:

Now that a gentler and more conventional policy prescription is close at hand, it may not frighten most readers away from the rest of the book to say that, yes, if one happens to be delicately balancing the arguments for and against revolution, the theory here does shift the balance marginally in the revolutionary direction.

In a way, we are converging on the orthodox Marxist view of the origins of the industrial revolution. Marx writes:

The revolutions of 1648 and 1789 were not English and French revolutions, they were revolutions of European significance. [...] the victory of the bourgeoisie meant at that time the victory of a new social order, the victory of bourgeois over feudal property, of nationality over provincialism, of free trade over the guilds, of subdivision of property over primogeniture, of landownership over the subordination of the owner by means of the land, of enlightenment over superstition, of the family over the family title, of industry over heroic idleness, of bourgeois right over mediaeval privileges.

But aren't we confusing cause and effect here? If these were bourgeois revolutions, weren't they only possible because the bourgeois had already gained sufficient power to achieve them? Olson in any case regards England as relatively stable.4 I leave the implications for the European Union as an exercise for the reader.

Wait a minute, this is completely insane!

Ah, well. Yes.

Maybe. Some of the arguments presented above are not exactly bulletproof. José Luis Ricón has a couple of good posts arguing against the idea that World War II caused an increase in growth. In The Productivity Impact of World War II Mobilization in the United States, Alexander Field argues that Gordon's estimates of growth from before the war are too low, and his estimates of growth after the war too high, so there's really no post-war boom at all.5 And with the increased destructiveness of modern warfare it is possible the calculus has changed completely.

Maybe it's just publication bias. There are thousands of destructive events; suppose 99% of them are genuinely bad, but we only get investigations of the remaining 1% because only the "good" ones can be turned into journal articles. One might argue that "destruction bad" doesn't get you published (though sometimes it does, eg terrorism bad for growth), while "destruction good" is exactly the type of contrarian bullshit beloved by academic economists the world over.

I'm not sure I buy that. Look, at least when it comes to destroying cities the mechanism isn't outlandish—there's path dependency that locks economic activity into suboptimal equilibria, and if you break out of them you can shift to more productive configurations. The power of agglomeration effects is extremely well-established. If you accept that (and you should), the only question left is whether the benefits actually exceed the costs. Now we're just haggling over the price, as Churchill said.

Scott Alexander is famously skeptical of systemic change and burning down the system. He writes:

Systems are hard. Institutions are hard. If your goal is to replace the current systems with better ones, then destroying the current system is 1% of the work, and building the better ones is 99% of it. Throughout history, dozens of movements have doomed entire civilizations by focusing on the “destroying the current system” step and expecting the “build a better one” step to happen on its own. That never works.

Yarvin responds to his fears by arguing that we can have bloodless systemic change and there's no need for fire at all. But the basic aversion to destruction goes unquestioned. "If all you have is a plan to “burn down the current system,” you do not actually have a plan at all", he says. I think they both underestimate the costs of being stuck in bad equilibria, and overestimate the pain caused by burning down the system. The problem with communist revolutions isn't the revolution, it's the communism.6

I started this essay with Bastiat, let's turn back to him again. In his famous essay, he contrasts that which is seen and that which is not seen: we observe the activity of the window repair, but not the opportunity cost.

To be ignorant of political economy is to allow ourselves to be dazzled by the immediate effect of a phenomenon; to be acquainted with it is to embrace in thought and in forethought the whole compass of effects.

What is seen is a disaster. What is not seen is the enormous damage caused every day by ossified structures that prevent economic activity from happening. Let us not be dazzled by the flames!

Samuel Hughes and Ben Southwood recently unveiled their policy proposal aimed at making Coasean bargains (for residential intensification) easier to realize, by distributing the gains to all local residents. The idea is to get everyone on a street together to agree to destroy it, then build up better and reap enormous profits. All I'm proposing is to do this at a slightly more ambitious scale.

Will it work? We won't know if we don't try. Let's start with a modest pilot program and tear down just one city, some place like Atlanta or Dallas. See what happens. Doesn't even have to be the whole metropolitan area, just a few key neighborhoods. You said you wanted progress studies, didn't you?

- 1.That is not to say that the fire was ultimately value-enhancing. The value of the lost goods is much greater. But those are simply incidental costs that could have been avoided had the fire been planned and controlled. ↩

- 2.Or even be involved in it directly? Sweden got a similar growth boost despite remaining neutral. Perhaps this should make us doubt the idea that the war caused the post-war growth? Or maybe they just benefited from a global wave of post-war growth that started in the countries actually involved. ↩

- 3.If the benefits of war are due to such as "reset", perhaps it's even preferable to lose a big war. ↩

- 4.He writes: "The logic of the argument implies that countries that have had democratic freedom of organization without upheaval or invasion the longest will suffer the most from growth-repressing organizations and combinations. This helps to explain why Great Britain, the major nation with the longest immunity from dictatorship, invasion, and revolution, has had in this century a lower rate of growth than other large, developed democracies." ↩

- 5.The differences in assumptions and their impact are neatly summarized in Table 3 on p. 49. ↩

- 6.Post-war East and West Germany offer an instructive example. ↩